MyFICO Premier identity theft protection review

Our Verdict

MyFICO monitors your credit and explains your credit scores meliorate than any competitors. But it offers just bones identity-theft-protection and fraud detection.

For

- Tops in credit monitoring

- Uses FICO credit scores

- Monthly 3-bureau credit reports

Against

- Lacks the latest identity-theft-protection features

- Quite expensive

Tom'southward Guide Verdict

MyFICO monitors your credit and explains your credit scores better than any competitors. Just it offers only bones identity-theft-protection and fraud detection.

Pros

- +

Tops in credit monitoring

- +

Uses FICO credit scores

- +

Monthly iii-bureau credit reports

Cons

- -

Lacks the latest identity-theft-protection features

- -

Quite expensive

MyFICO Premier: Specs

Frequency of credit reports: Monthly

Frequency of credit scores: Monthly

Credit-improvement simulator: Yeah

Address-change monitoring: No

Data breach alerts: No

Investment account monitoring: No

Medical records monitoring: No

Payday loan monitoring: No

Sex offender alarm: No

Security software: None

Championship-change alerts: No

Two-factor authentication: No

MyFICO Premier offers the best credit monitoring of any service we've tested. But it's not primarily an identity-theft-protection service, and in fact offers only the basics of identity monitoring and fraud detection. Instead, it's all-time for customers who want to concentrate on their credit scores.

What MyFICO does requite you is monthly access to credit reports and the FICO credit scores derived from them, besides as how those scores are calculated and what you lot can exercise to alter them.

FICO scores are used past most lenders to determine your creditworthiness for loans, credit cards and mortgages. Other services show yous credit scores that effort to lucifer FICO scores, merely MyFICO gives you the existent deal.

In terms of identity theft protection, MyFICO is solid but not the best. It monitors your banking concern accounts, court records and the "night web," but it tin can't catch accost changes, home-title theft or information breaches and offers no protection from malware or phishing.

Nosotros'd give MyFICO Premier a college rating as an identity-theft-protection service if it had a few more of those abilities. As a credit-monitoring service, it tin can't exist beat.

For the best identity-theft protection, endeavour IdentityForce or LifeLock. Only if you care more well-nigh your actual FICO credit scores than anything else, so MyFICO will deliver.

Read on for the balance of our MyFICO review.

MyFICO: Costs and what's covered

An adjunct of Fair Isaac Corp (aka FICO), the originator of modern American credit scores, MyFICO focuses on FICO credit scores and ignores some of the mainstays of identity protection. That makes it good if you want data pertinent to taking out a loan, merely bad if you want a total suite of identity-theft-protection services.

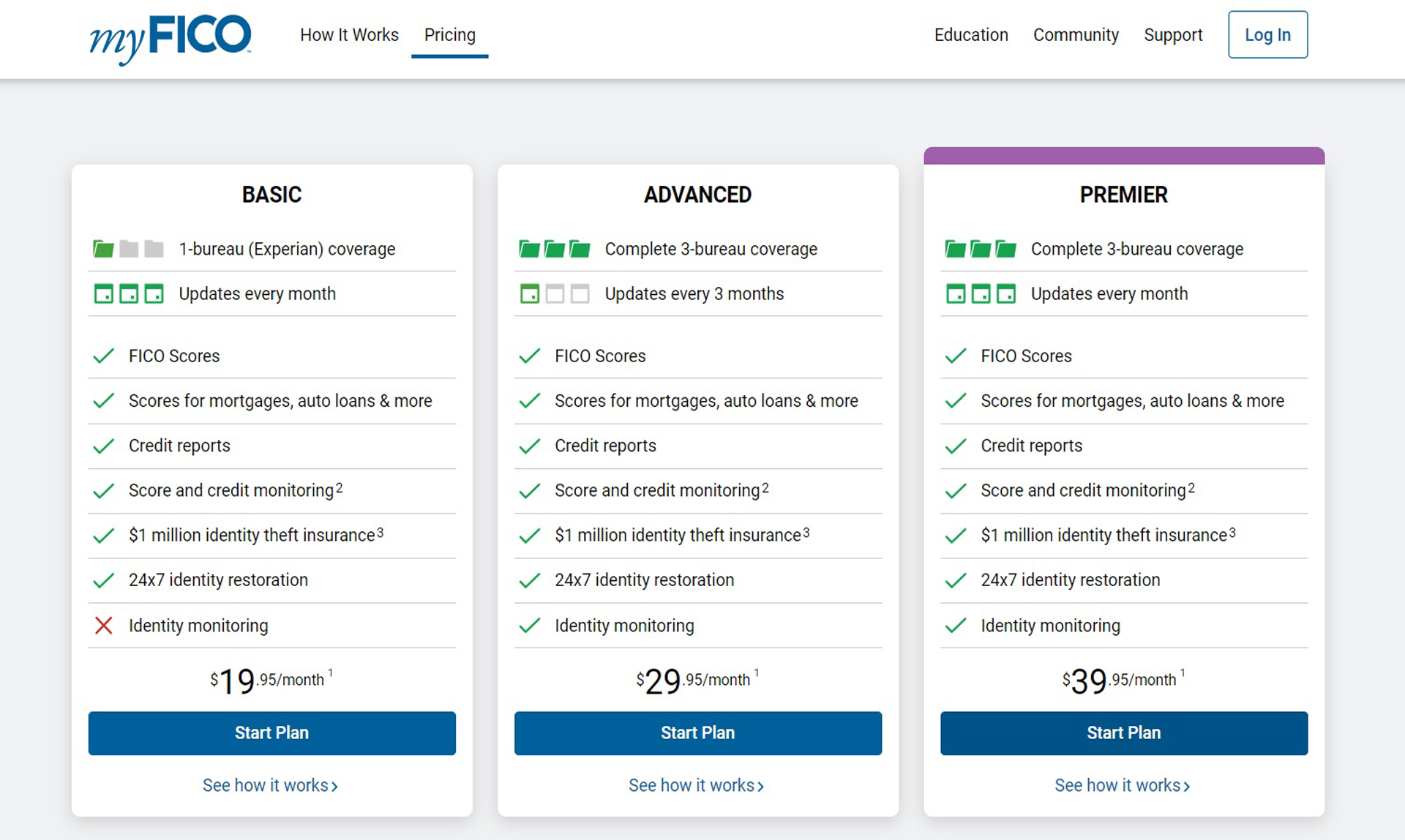

MyFICO has 3 service plans, starting with the $20-a-month Bones program. Information technology includes admission to 10 different FICO credit scores, including those used for mortgages, automobile loans and credit cards. Y'all get monthly credit reports from Experian too as monthly FICO credit scores and alerts if there are whatever changes.

The Basic program includes $1 million of insurance to restore your credit and identity if it is stolen while on MyFICO's spotter. Even so, it lacks any monitoring of identity data, such as whether some of your data is existence offered for auction in "dark spider web" marketplaces.

MyFICO's Advanced plan costs $xxx a month. It includes full credit reports from the big three credit bureaus — Equifax, Experian and TransUnion — as well every bit the 28 about used FICO indicators. The credit reports arrive quarterly, and the service as well includes monitoring of your personal data on the open and night web.

That frequency of credit reports and scores is unusually generous for a mid-priced programme in this category. But IdentityForce's top-end plan gives you like credit monitoring plus more than identity-theft-protection features for $24 a month.

There'south likewise a Family version of the MyFICO Advanced programme that covers ii adults and equally many as ten children upwardly to age 18 for $l a month. By dissimilarity, Identity Force's unlimited family plan costs $fourteen less.

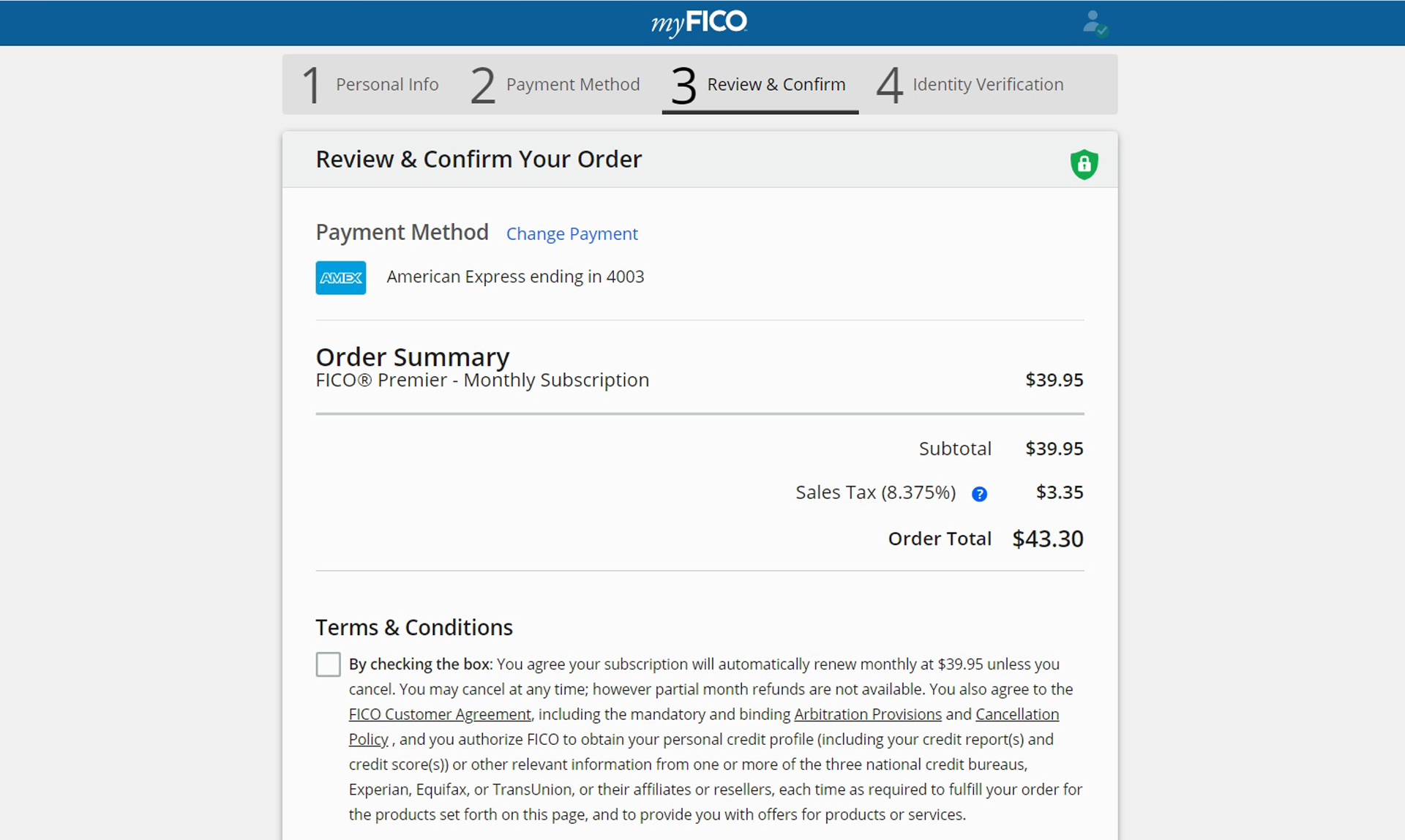

The Premier program is MyFICO's most expensive plan.,At $40 a month, it costs more than any other credit-monitoring or identity-theft-protection plan we've reviewed. MyFICO Premier ups the frequency of credit reports from quarterly to monthly simply otherwise matches the Avant-garde plan.

All of the MyFICO plans get sales taxation added to the advertised cost, in my example 8.25%. In that location's no discount for paying for a year at in one case, and as a result, MyFICO Premier volition run you $480 per year. LifeLock Ultimate Plus, which includes the full Norton 360 Deluxe security suite and has many more identity-monitoring tools, although far less credit monitoring, goes for an almanac $350.

MyFICO has an A+ rating from the not-profit Better Business Agency. When we terminal looked, in that location were 27 complaints, most of which had detailed responses from the company. MyFICO rated a 3.25 out of 5 from ConsumerAffairs, which is paid past some of the companies whose products it reviews.

| MyFICO Basic | MyFICO Advanced | MyFICO Premier | |

| Monthly toll | $20 | $thirty | $40 |

| Yearly toll | $240 | $360 | $480 |

| Family programme | None | $50, two adults & upwards to 10 kids | None |

| Credit reports provided | Experian | Equifax, Experian, TransUnion | Equifax, Experian, TransUnion |

| Credit bureaus monitored | Experian | Equifax, Experian, TransUnion | Equifax, Experian, TransUnion |

| Frequency of credit reports & scores | Monthly | Every three months | Monthly |

| Type of credit score | FICO | FICO | FICO |

| Credit-comeback simulator or advice | Yes | Yes | Yes |

| Bank, bill of fare accounts monitored | No | Aye | Yes |

| Black-market ("dark spider web") monitoring | No | Yes | Yes |

| Lost wallet assistance | Yep | Yes | Yeah |

| Court record monitoring | No | Yes | Yes |

| Max. ID-theft coverage | $1 one thousand thousand | $ane million | $one one thousand thousand |

MyFICO: How we tested

In the late summer of 2020, I signed up with five of the biggest identity-theft-protection services, including the MyFICO Premier service plan. All were paid for by me and reimbursed by Tom's Guide.

Afterwards I installed the MyFICO mobile app on my Samsung Galaxy Note twenty, I logged on most days over the form of 3 months. In improver to checking on Premier's alerts, notifications and changes to my credit and identity, I checked my credit scores.

I used the credit simulators and utilities, but as MyFICO doesn't include antivirus or security software on whatsoever of its plans, I couldn't evaluate those. Finally, I checked in with each company's support staff and recorded how long it took them to respond. At the end, I canceled the service.

MyFICO: Credit scores and monitoring

The MyFICO services focus sharply on FICO credit scores and monitoring. Few other identity-theft-protection or credit-monitoring service provides your bodily FICO scores, which most banks and other lenders use to determine your creditworthiness. FICO scores are accessed millions of times a solar day and are key indicators for 90% of U.S. lending decisions.

Most identity-theft-protection services instead use the VantageScore 3.0 credit scores, issued past a company jointly owned by the Big Three credit bureaus Equifax, Experian and TransUnion. VantageScore 3.0 scores only approximate FICO scores but are sometimes used by lenders.

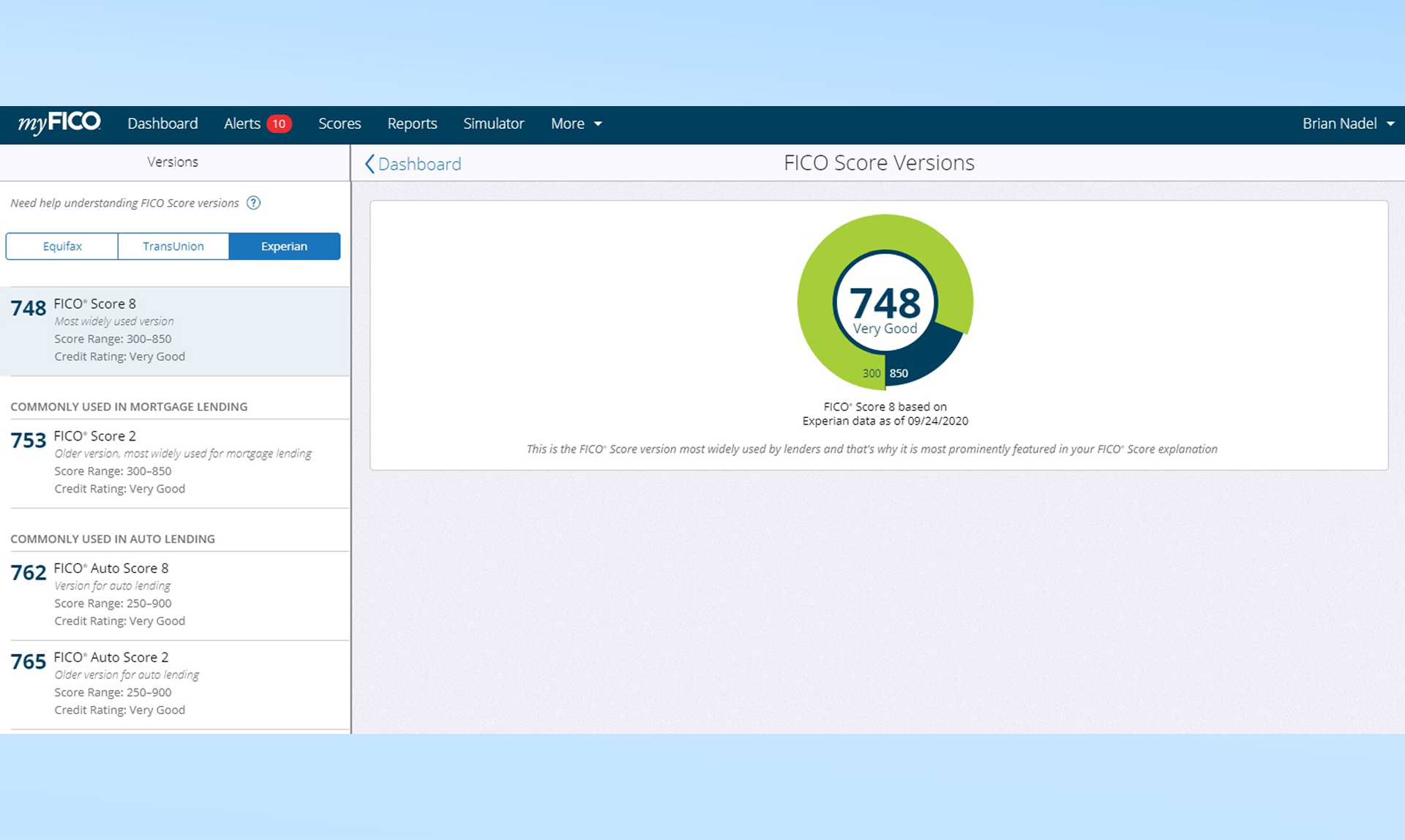

Because FICO provides more than 2 dozen credit scores, it can be a bit much for the uninitiated. For example, the FICO 2, 4 and 5 scores apply data from Experian, TransUnion and Equifax, respectively, for banks to determine creditworthiness for a mortgage.

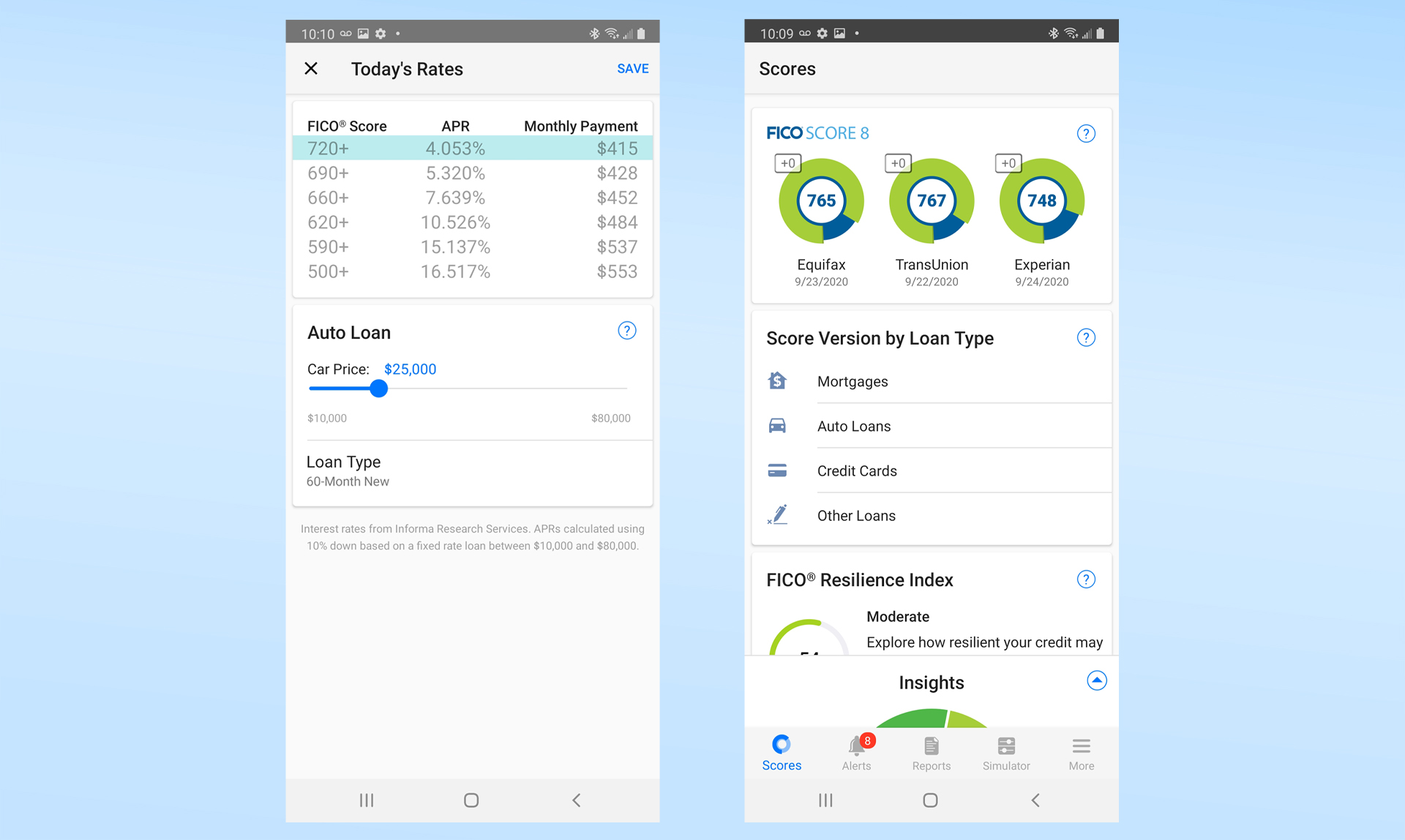

The FICO 8 score uses data from all 3 credit bureaus and is for car loans and credit cards. The FICO 9 score is new and is growing in popularity. MyFICO shows you all these and other FICO scores.

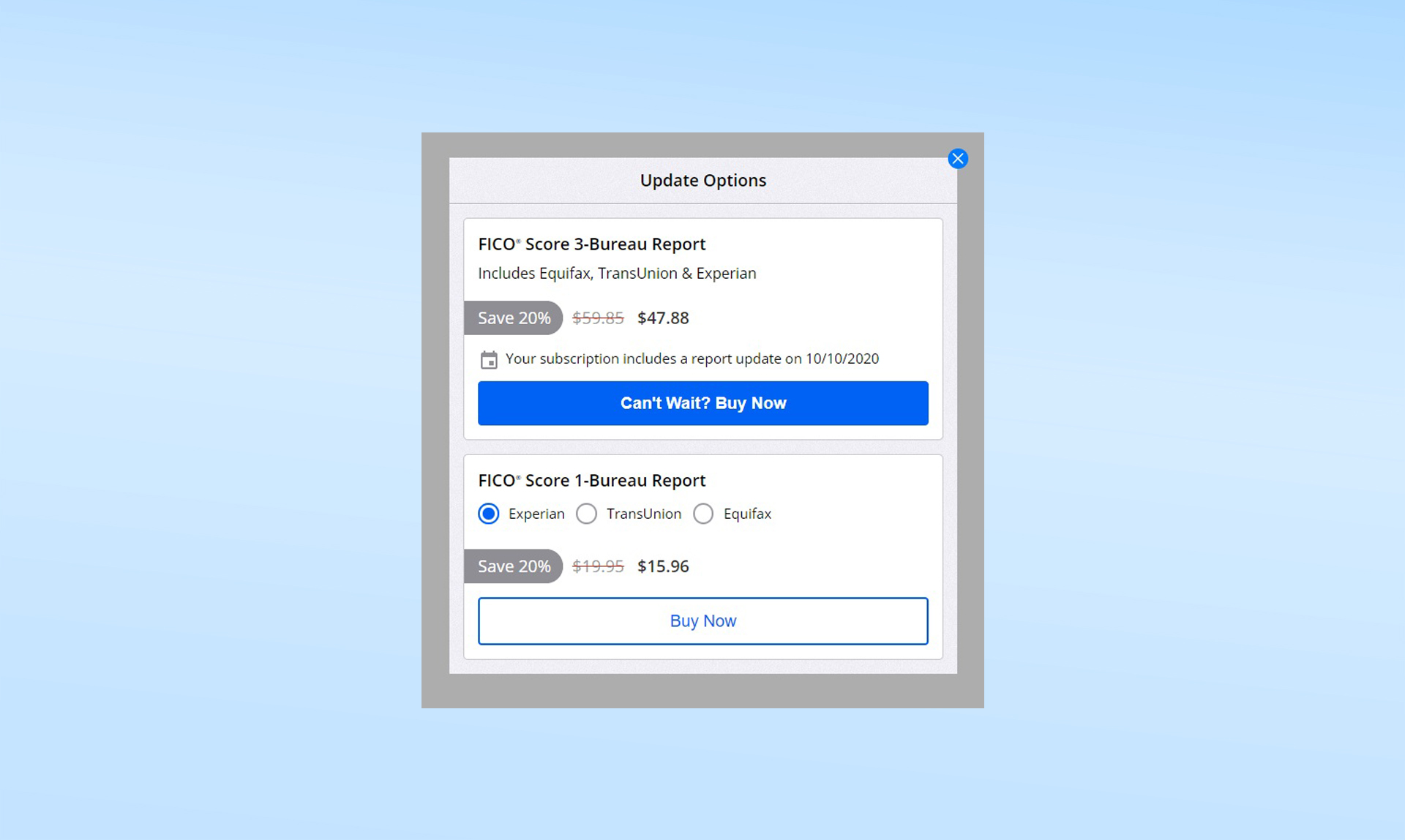

With the MyFICO Premier plan, yous go access to the total credit reports from all 3 credit bureaus every calendar month. Most identity-theft-protection services provide credit reports simply annually or quarterly. MyFICO also lets yous purchase instant reports — $sixteen for a single bureau's study or $48 for all three.

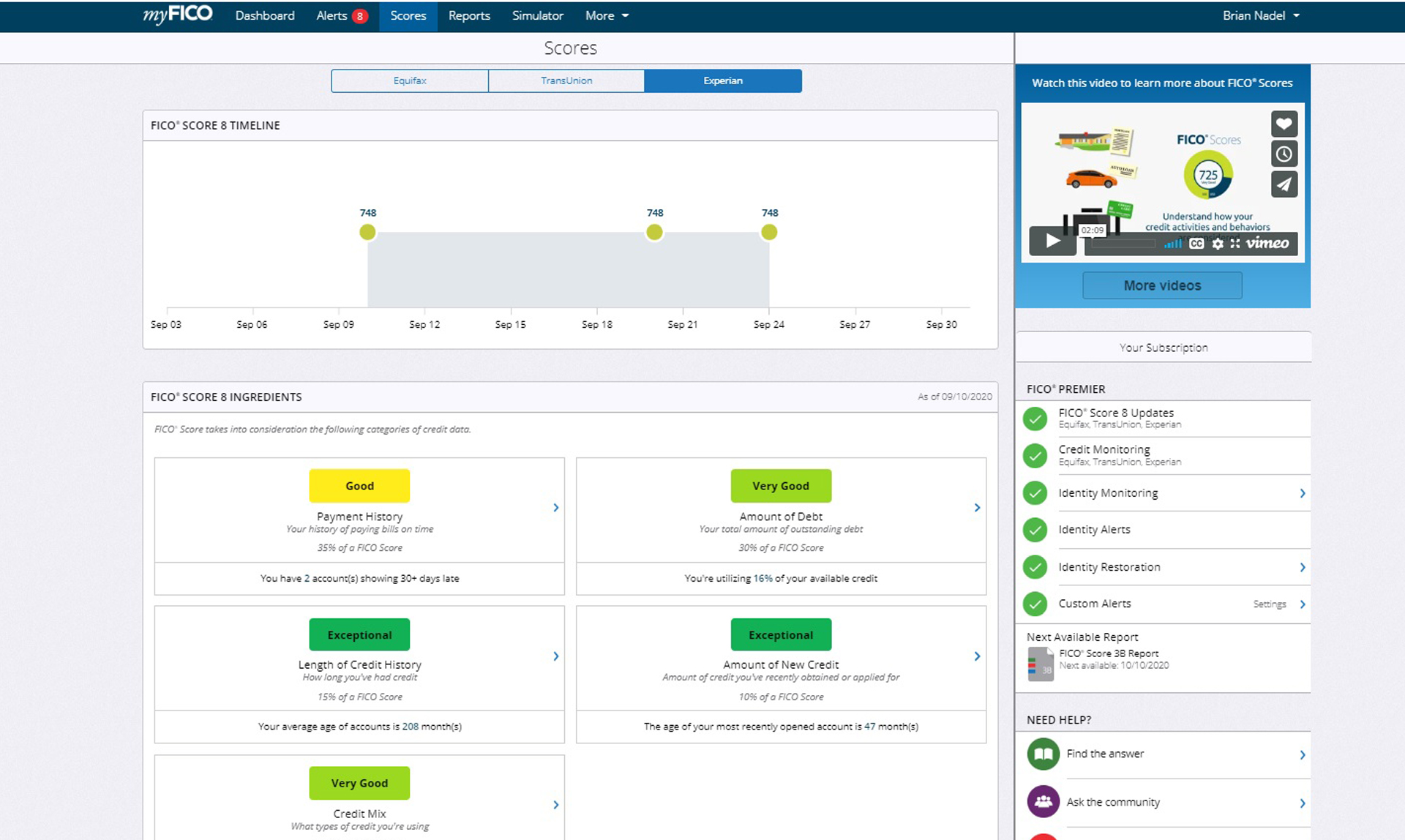

Almost identity-protection service take a credit-score tracker that graphs your credit ratings over time, but MyFICO adds a twist. It provides an appraisal of the ingredients that get into each FICO score to provide more insight into how the scores are formed. These factors can include payment history, debt load, length of credit history and the mix of credit sources.

The MyFICO Advanced and Premier plans go on an middle out for instances of your personal data showing upwardly online and on the dark Web. They monitor public records, such state and federal courtroom proceedings, and tin can spot sudden changes in your credit-menu balances as well as new accounts created in your name. But they don't track human activity or title changes for your dwelling and can't see if someone has inverse your accost with the U.S. Postal Service or filed tax returns in your name.

MyFICO: Insurance and services

Similar many of its peers, MyFICO seeks to help you with lawyers, investigators and experts to get your identity and credit dorsum in case your identity is stolen under its sentry. Information technology also has a $1 million insurance policy, underwritten by American Bankers Insurance Company of Florida, that can be usedto recover lost funds that a depository financial institution or credit card visitor won't cover.

The insurance policy tin also reimburse yous for expenses for travel, certificate notarization and loss of wages related to your example. MyFICO will pay y'all for your entire actual lost revenue upward to the policy limit.

MyFICO: Notifications and alerts

MyFICO posts alerts for you in its desktop-browser interface and its mobile apps, but also sends SMS text-message alerts to your cellphone number as well equally emails. However, it plans to phase the texted alerts out due to low need, which is a shame considering those kept me focused on the alerts. The service'south notifications were the about detailed of the 5 identity-theft-protection services we've recently reviewed.

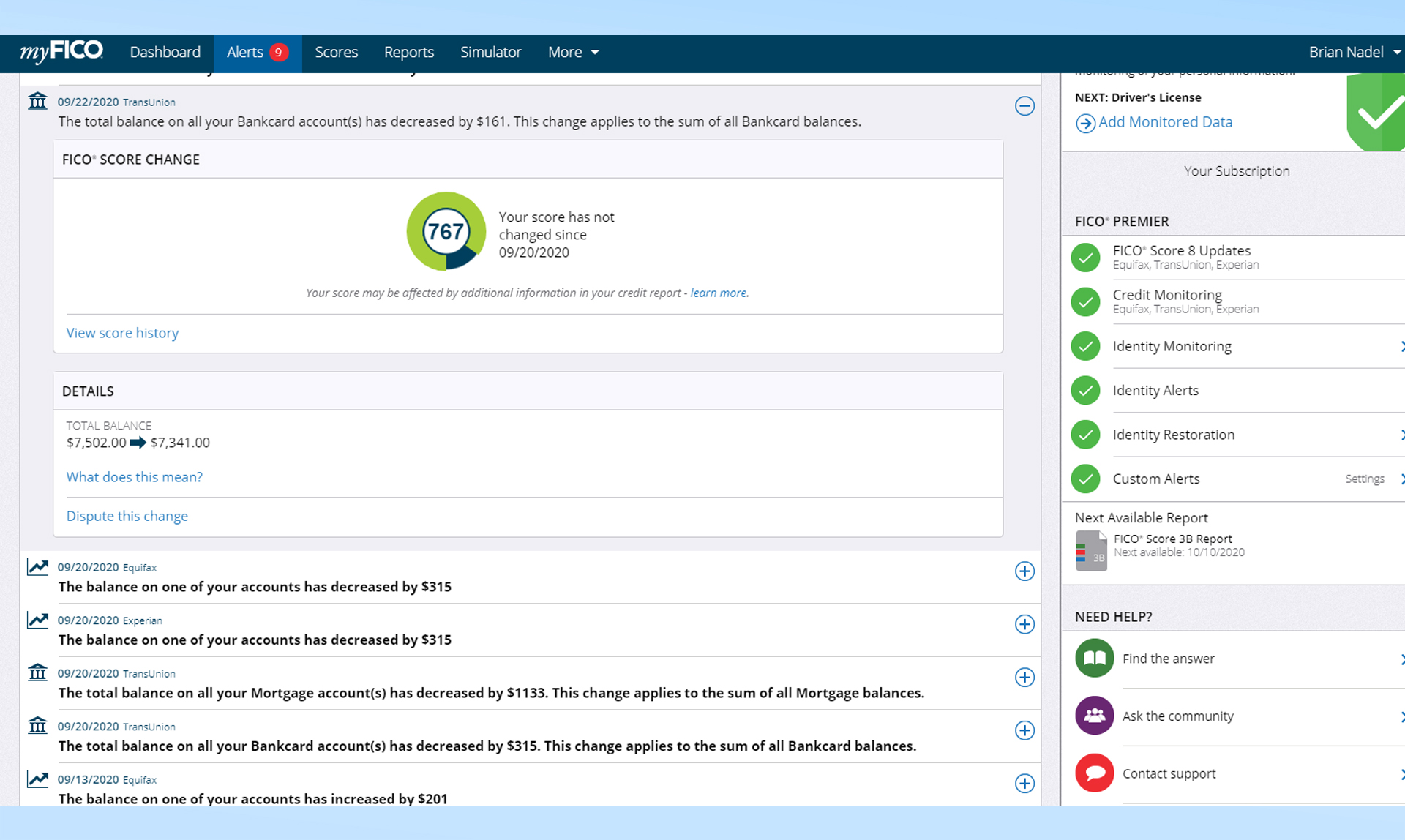

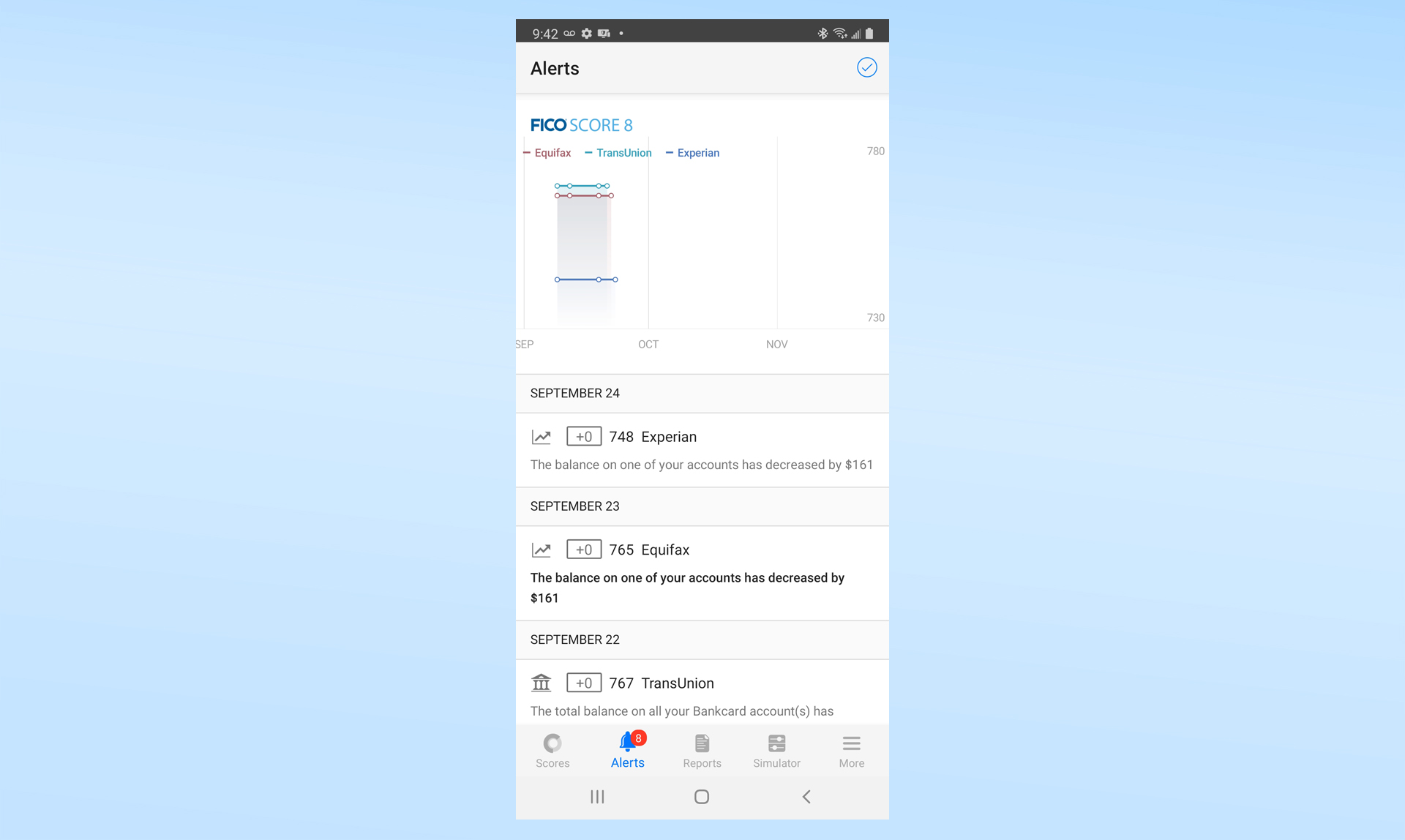

Exist warned — the alerts can be overwhelming. Over my three-month test period, I received dozens of notices from MyFICO that my credit-card balance was rising while my banking company account was falling. The alerts more often than not came in batches of 3 — 1 from each credit bureau.

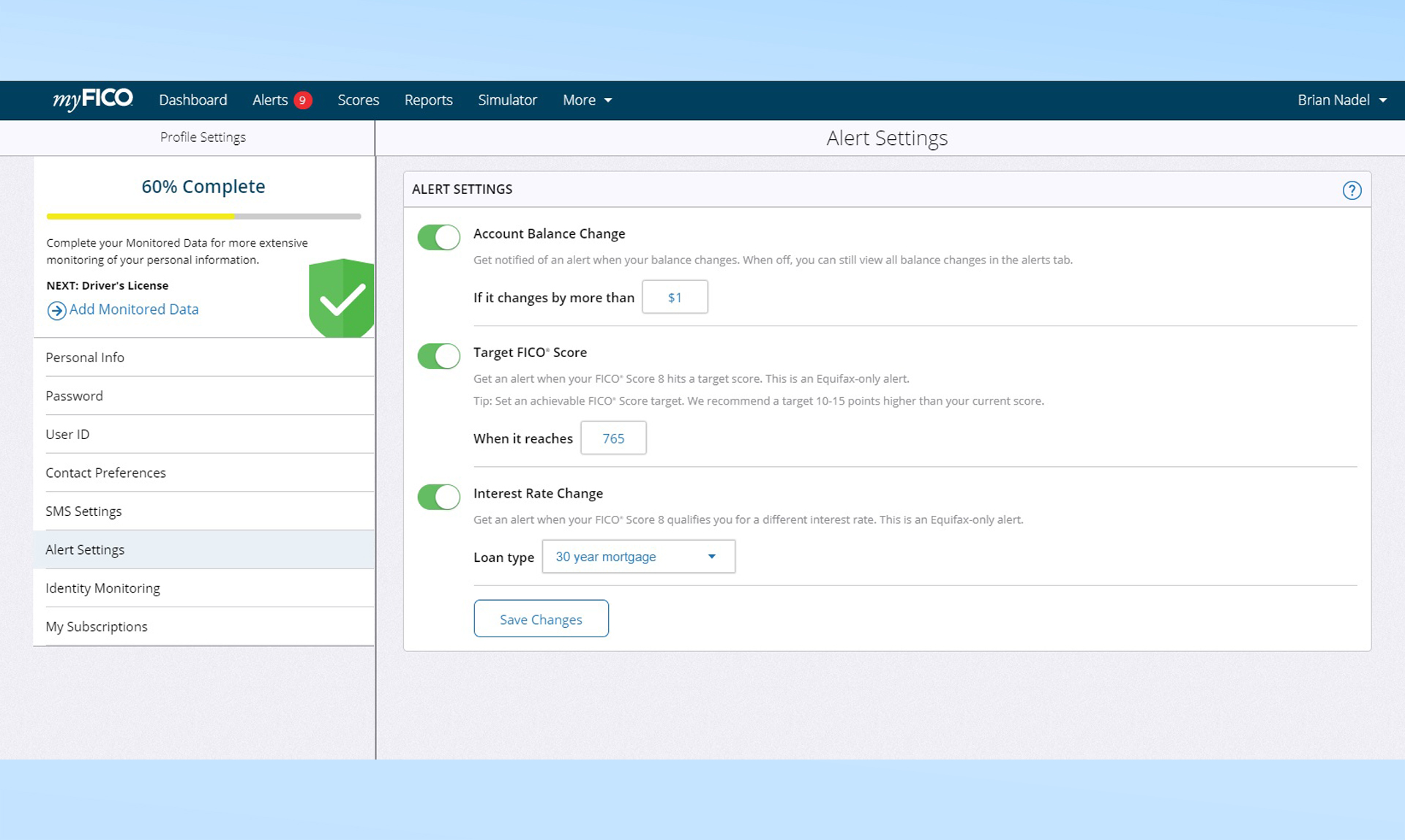

Unfortunately, MyFICO's default setting is to send out an warning if any account balance changes by $1. Once I figured this out, I adjusted the threshold and was less often bothered.

MyFICO also has a hidden bonus quirk that might help anyone considering refinancing a mortgage. Its Custom Alerts department can be set to send an alarm when your FICO score changes to qualify y'all for a lower interest rate.

Overall, I received 54 alerts from MyFICO via the online interface, texts and the mobile app over the class of three months, by far the nearly alerts of any of the v identity-theft-protection services I recently reviewed. All the alerts from MyFICO were specific, although some were puzzling at first. Setting up a mortgage yielded credit inquiries from Factual Data, a company that works as a data broker for the credit agencies, but the warning made no mention of the words "mortgage" or "loan". There's a link in the MyFICO alert notifications to dispute a change.

MyFICO: Setup

Getting started with MyFICO was generally efficient, simply a couple of glitches got in my way and the entire setup process took more an hour. Afterwards I went to the MyFICO site and picked the Premier plan, I needed to enter an e-mail address and password for the account. If you lot don't desire to receive promotional and marketing material from MyFICO, be sure to click the opt-out box.

I and then needed to fill up in my personal information, but the MyFICO site balked at letting me enter the town and state I live in; it took 2 tries to finally get it to piece of work. The site wanted payment information from a credit card or PayPal account, and I filled in my data.

Unfortunately, the payment data got caught in a processing loop and I gave up subsequently 15 minutes. I sent MyFICO'south tech-support people an email and got a reply that the payment was not complete and to effort once again. I did and two minutes later, it was accepted.

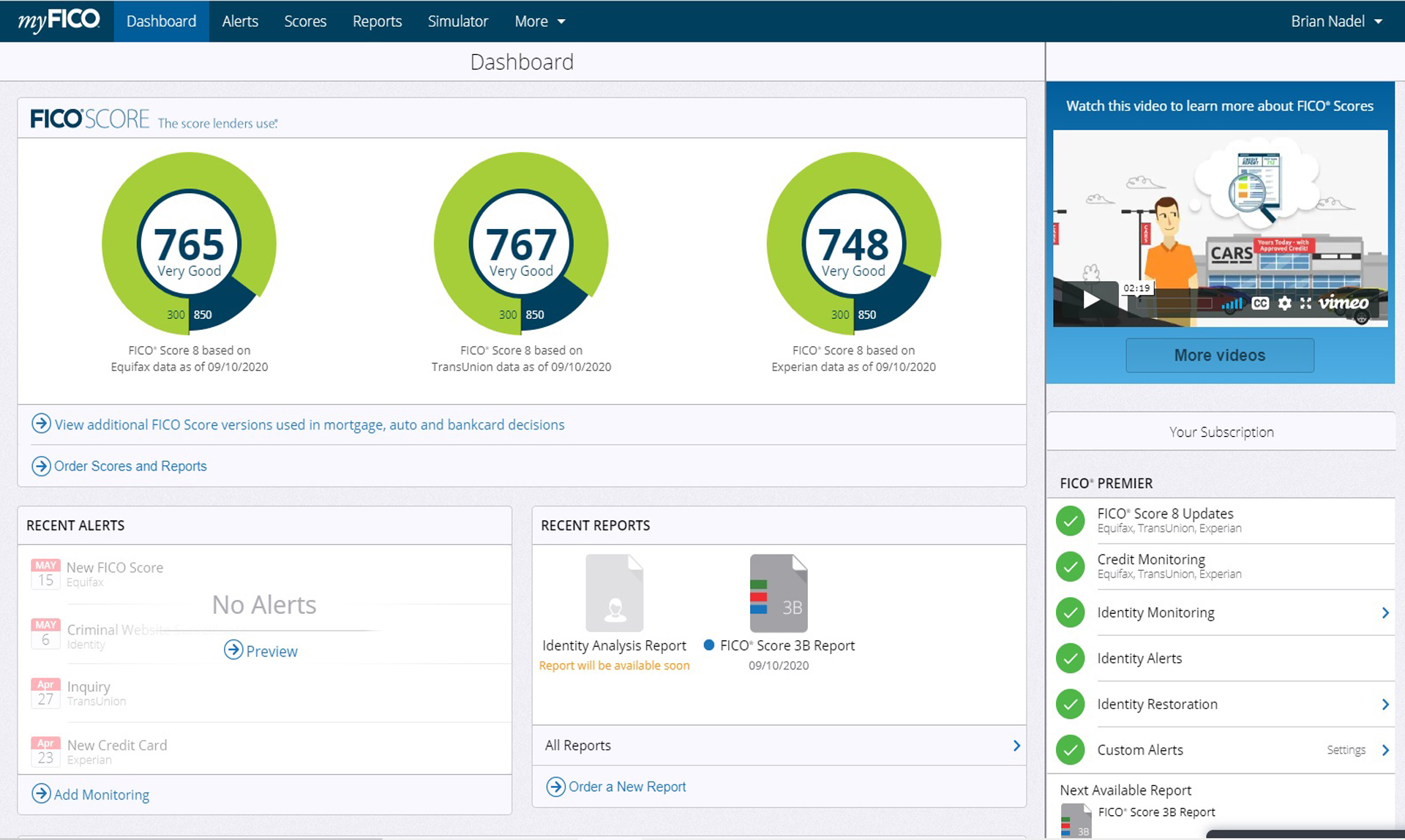

I now had to evidence my identity by answering four questions about my life, including queries about past and present addresses, mortgages and credit cards. I passed and was sent to the service's Dashboard, which showed me my FICO scores for all three bureaus. The whole process took 1 60 minutes and 15 minutes, although my problems might have been unique.

The adept news is that, co-ordinate to MyFICO, all my personal data was transported dorsum and forth and saved in encrypted form. The company promises to wipe all your information after cancellation, but it lacks two-factor hallmark to protect your account in case someone steals your password.

MyFICOs has identity-restoration experts on phone call 24/vii, only its general customer-support coiffure is available only Mon through Fri from 6:00 a.m. to 6:00 p.m. (Pacific time) and Saturday from 7:00 a.m. to 4:00 p.m. The site has informational videos about the MyFICO the service, including 1 about how the FICO score is generated.

There's a direct link from the MyFICO browser interface to the support site and a quick way to send client support an e-mail. On the other paw, the customer-back up phone number is especially well hidden on the website, and information technology took customer back up three.v hours to respond to a pricing problem I had.

MyFICO: Interface and utilities

MyFICO combines a thorough online interface with a practiced mobile app, and both provide like information. The app requires the utilise of a Pin, a fingerprint or facial recognition to apply, while the online version requires a full log in with the account's username and password.

That said, MyFICO'south browser-based interface needs to be zoomed out to 50% or scrolled up and downwards a lot to see all the data presented. The chief Dashboard page lists your FICO 8 scores forth with the data they're based on. Below that is admission to other FICO scores. Click on any of them and y'all'll observe a dainty tracker and overall appraisal of your creditworthiness. The Dashboard as well lists recent alerts and credit reports.

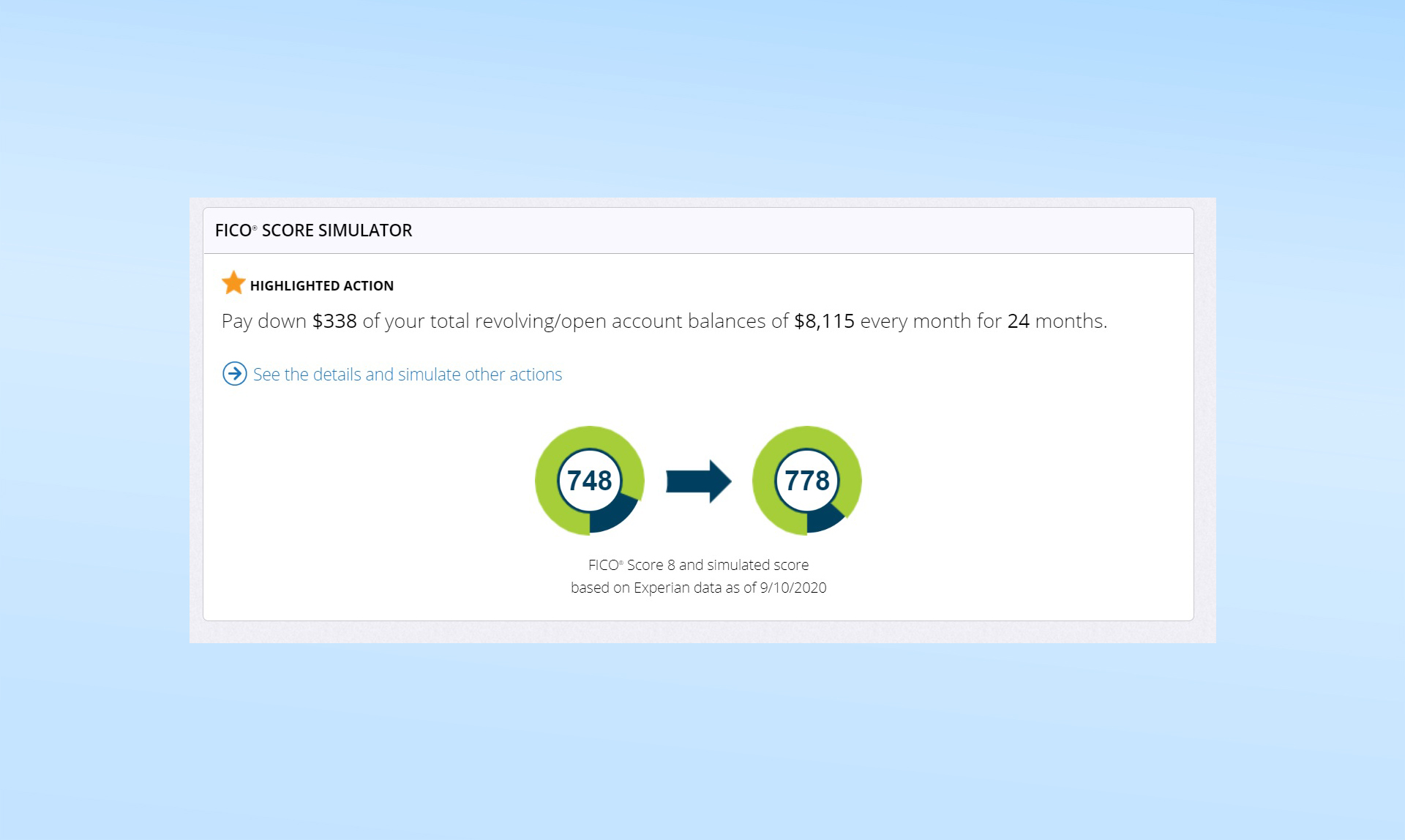

MyFICO's killer characteristic is its FICO Score Simulator. Other identity-protection services can merely estimate nearly the hugger-mugger sauce that's used to plow raw credit data into a real FICO score, but MyFICO knows the verbal algorithms.

In other words, MyFICO tin can accurately model changes to predict your resulting credit score more closely and also proactively requite y'all tips. For instance, rather than waiting for me to submit possible changes so telling me what my credit score might be later, the MyFICO simulator suggested that I lower my credit-card rest by $338 to raise my credit score by 30 points.

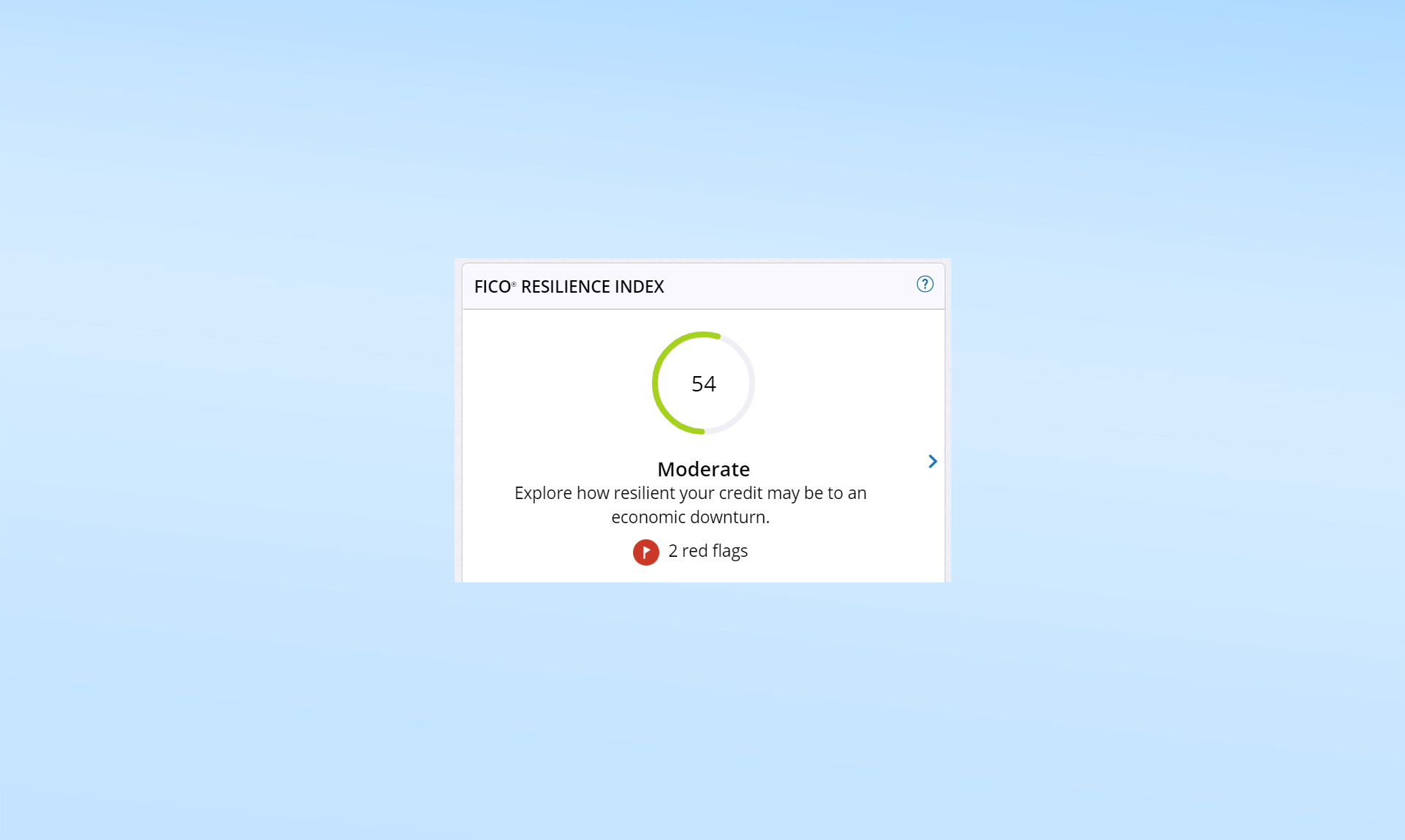

The FICO Resilience Alphabetize is used by lenders to aid predict how resilient a person's credit may be in the issue of an economical downturn. It showed ii red flags nigh my credit that might bear upon my score.

On the downside, MyFICO lacks actress security software like LifeLock's Norton 360 antivirus suite or Identity Guard's browser extensions. If yous're happy with your existing security software, then this will be fine, but those extras provide an additional layer of protection, often at a disbelieve, to anyone who doesn't already have them.

MyFICO's Android and iOS apps squeeze a lot into a minor screen. Along the top of their forepart pages are the three credit-agency FICO scores along with their concluding updates, followed by access to the unlike FICO scores for everything from getting a mortgage to a machine loan.

The loan and mortgage calculators that use estimated rates based on your credit scores are bachelor in both the apps and the online browser interface.

As the leader in credit scoring, Fair Isaac has a large Education section on the MyFICO site. The section has a Q&A section to explain FICO scoring and lots of information well-nigh how to amend credit scores and how to right errors. My favorite office was the glossary that defined many key credit terms most people have never heard of.

MyFICO: Counterfoil

Getting free of MyFICO can exist done by calling its hotline or using the My Subscriptions portion of the interface. At the bottom right of the front folio is a spot to abolish your subscription, but be gear up for an ominous warning about the grave consequences of your decision.

I got an on-screen confirmation of my MyFICO cancellation too as an emailed confirmation, but the cancellation didn't take effect until the terminate of the current billing cycle.

MyFICO review: Bottom line

MyFICO Premier'southward ability to provide the verbal criteria used by banks and credit-card companies to determine your credit scores is refreshing and useful, but the 28 unlike FICO scores y'all see can be too much.

The service as well lacks many of the mainstays of identity-theft-protection, such as alerts nearly address changes and information breaches. For those, we recommend IdentityForce UltraSecure + Credit or LifeLock Ultimate Plus. And while MyFICO's family plan lets you cover a lot of children, so do other services that toll much less.

But if you want to stay laser-focused on your FICO credit scores, how they're used and how to make them better, and so MyFICO is for you.

Source: https://www.tomsguide.com/reviews/myfico

Posted by: keithberch1963.blogspot.com

0 Response to "MyFICO Premier identity theft protection review"

Post a Comment